📊 The ROIC Ratio: How to Tell If a Company Actually Creates Value

Why earning a profit isn't enough — the real test is beating your cost of capital.

explained by The Yield Dealer")

When you analyze a stock, it’s tempting to focus on the visible numbers: revenue growth, net income, margins, the dividend, the share price. Useful — but they don’t answer the question that matters most: is the company using its money efficiently?

That’s exactly where ROIC comes in.

What is ROIC?

ROIC (Return on Invested Capital) measures how well a company generates profit from the capital actually put to work in its business. In other words: does it turn the money invested in its factories, inventory, software, brands, acquisitions, and day-to-day operations into real economic profit?

It’s a favorite of long-term investors because it goes beyond accounting profit — it tries to measure the deep economic quality of a business.

A simple idea behind a technical formula

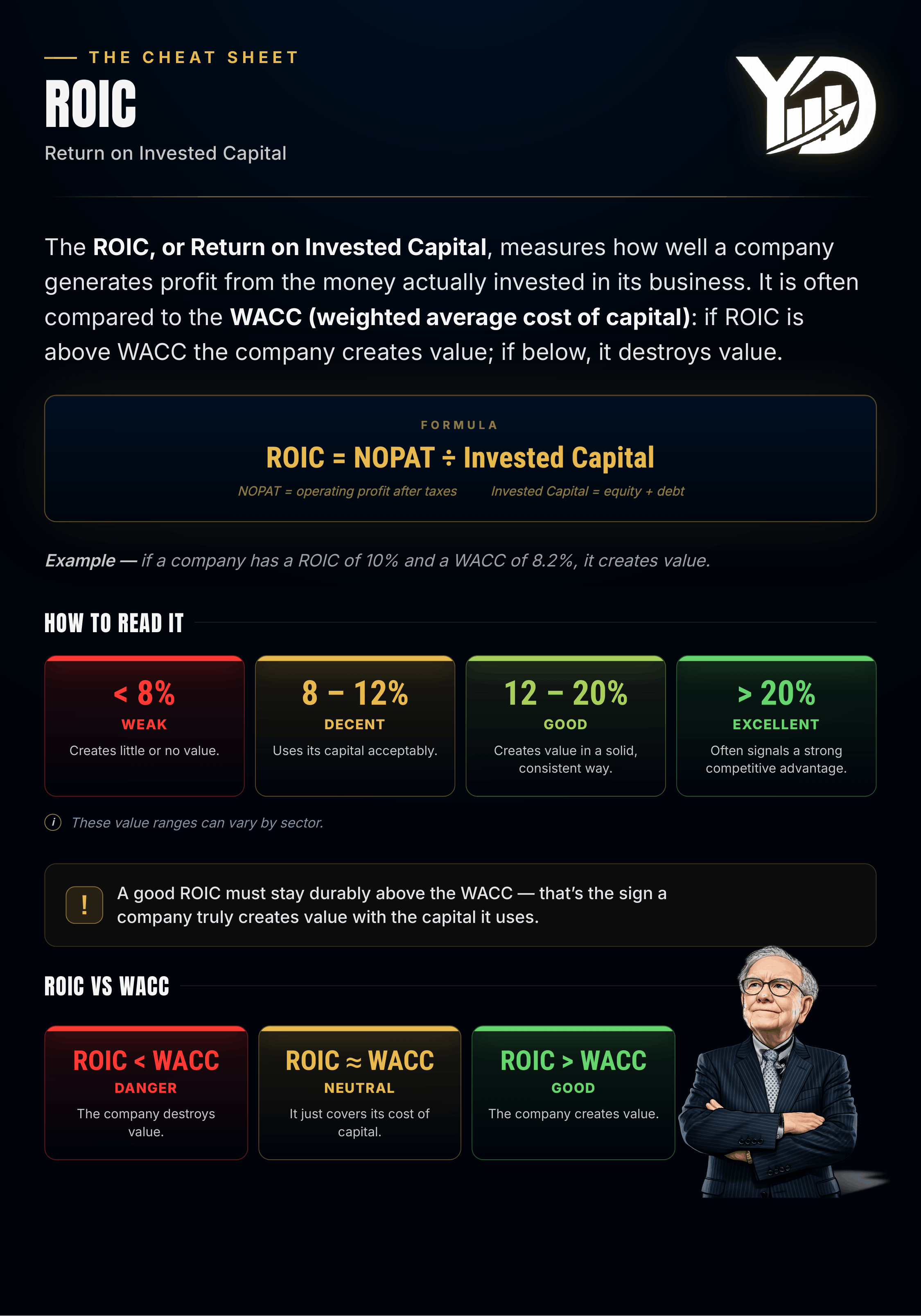

Formula: ROIC = NOPAT ÷ Invested Capital

NOPAT = operating profit after taxes. It’s the profit from the core business, after a theoretical tax charge but before financing choices — so you see operating performance regardless of whether the company is funded by debt or equity.

Invested Capital = the resources used to run the business. Usually calculated as equity + net financial debt, or as operating assets minus operating liabilities (like payables).

Behind the jargon, the idea is intuitive. A company raises capital — from shareholders, lenders, or reinvested profits — and the question is simply: how much operating profit does it produce with it?

Example: A company generating $10 of after-tax operating profit on $100 of invested capital has a ROIC of 10%. One generating $5 on the same capital has a ROIC of 5%. The first uses its capital better — all else equal.

Why ROIC matters so much

ROIC gets to the heart of value creation. A company doesn’t create value simply because it makes money. It creates value when it earns more than its capital costs.

This is where you compare ROIC to the WACC (Weighted Average Cost of Capital) — the blended cost of the company’s funding from both shareholders and lenders.

ROIC above WACC → the company creates value. It earns more on its capital than that capital costs.

ROIC below WACC → it destroys economic value, even if it’s still profitable on paper.

A company doesn't create value simply because it makes money. It creates value when it earns more than its capital costs.

Example: A ROIC of 12% against a cost of capital of 8% is favorable — every dollar reinvested earns more than it costs. But a ROIC of 6% against a 9% cost of capital doesn’t cover the cost of the resources used. The company can keep growing, but that growth risks destroying shareholder value.

That’s why the best companies aren’t just the ones that get bigger — they’re the ones that grow while maintaining a high ROIC.

What’s a good ROIC?

There’s no universal threshold — it depends heavily on sector, business model, competition, capital intensity, and the economic cycle. That said, some rough benchmarks:

Below 8% — often weak, especially if the cost of capital is close to or above that. May signal poor capital use, brutal competition, or heavy low-return investment.

8 – 12% — can be acceptable, but analyze with care. The company may cover its cost of capital without any obvious competitive edge.

12 – 20% — more interesting. Often suggests good operating efficiency, disciplined capital allocation, or a solid competitive position.

Above 20% — potentially excellent. Can reflect a strong brand, an asset-light model, pricing power, scale effects, or a high barrier to entry — but always verify it isn’t temporary or built on an unusually small capital base.

The level at a single point in time isn’t what matters most. Consistency over time is.

Durability beats the number itself

A high ROIC in a single year doesn’t make a company exceptional. Favorable conditions, a temporary price spike, a cost dip, or a period of under-investment can all flatter it briefly.

Look at ROIC over several years. A company that sustains a high ROIC for five, ten, or fifteen years usually proves something deeper: it has a competitive advantage — a moat.

That moat can take many forms: a powerful brand that commands premium prices, a network that’s hard to replicate, proprietary technology, loyal customers that lower acquisition costs, a dominant platform with network effects, or an asset-light model that produces a lot of profit with little capital.

That’s what quality investors hunt for — not just a business that’s profitable today, but one that can reinvest its profits at high rates for a long time.

High ROIC + growth: the most powerful combination

ROIC becomes especially powerful alongside good reinvestment opportunities.

A company with a high ROIC but few places to reinvest can still be an excellent mature business — it generates lots of cash and returns it via dividends or buybacks. That’s already attractive.

But the most compelling case is a company that can reinvest a large share of its profits at a high ROIC. There, compounding becomes very powerful: future earnings can grow strongly without issuing much stock or piling on debt. It’s one of the classic recipes behind great long-term stock performance.

The reverse is dangerous: a company growing fast at a low ROIC consumes capital — new stores, new factories, more inventory, acquisitions — but each dollar invested earns little. Revenue growth can mask weak value creation. In the market, not all growth is worth having: profitable growth is worth far more than growth bought through poor capital allocation.

What ROIC reveals about management

ROIC is also an indirect read on management quality. Good managers don’t just grow sales — they decide where to invest, how much, what price to pay for acquisitions, when to buy back stock, when to cut debt, and when to return capital.

Capital allocation is one of a leader’s most important jobs. A great core business can still destroy value through overpriced acquisitions, low-return projects, or excessive debt in pursuit of poorly managed growth.

A durably high ROIC suggests the team invests wisely. A steadily declining ROIC can warn that the company is pouring money into less profitable projects, overpaying for deals, or watching its moat erode. ROIC isn’t only a financial measure — it’s a gauge of strategic discipline.

The limits of ROIC

Like any ratio, ROIC should never be used alone.

⚠️ Sector distortions. Capital-heavy industries — energy, telecom, heavy manufacturing, transport, real estate, semiconductors, utilities — must invest massively to operate, so their ROIC is structurally lower. Comparing a power producer’s ROIC to a software company’s makes little sense. Compare close peers.

⚠️ Accounting effects. Invested capital is affected by acquisitions, writedowns, goodwill, depreciation policy, and buybacks. Two economically similar companies can show different ROICs purely from accounting history.

⚠️ Intangibles. Heavy spending on R&D, marketing, and brand is often expensed rather than capitalized. That can make invested capital look smaller than it economically is — inflating the apparent ROIC. Common in tech, pharma, software, and branded consumer names.

⚠️ Cyclical businesses. In commodities, autos, construction, or shipping, ROIC swings with the cycle — excellent at the peak, poor a few years later. Look at average ROIC across a full cycle.

⚠️ Under-investment. A company can temporarily boost ROIC by deferring necessary maintenance or under-investing in the future. The ratio looks better while future competitiveness quietly erodes.

How to use ROIC in your analysis

For an individual investor, ROIC works best as a quality filter — a way to flag companies worth deeper analysis.

Look at several things together: the ROIC level over recent years, its trend, its stability, its spread over the cost of capital, the company’s growth, and its ability to reinvest at attractive rates.

High and stable → generally a good sign.

High but declining → pay attention.

Low but improving → potentially interesting in a turnaround, but higher risk.

Below the cost of capital for years → often a real concern.

Then read the annual reports to understand where the ROIC comes from: high margins? low capital intensity? pricing power? fast asset turnover? a dominant brand? hard-to-copy technology?

The ratio raises the alert; the analysis explains why.

Don’t overpay for quality

A high-ROIC company is often a high-quality company. But that doesn’t automatically make the stock a good buy at today’s price. Valuation still matters.

An excellent business can be a poor investment if bought far too expensively. A mediocre one can occasionally be an opportunity if bought very cheaply — though that demands more caution.

ROIC helps you judge the quality of the business. It doesn’t tell you whether the price is right. For that you also need valuation, growth prospects, future margins, risk, financial structure, and the expectations already baked into the share price. A high ROIC often justifies an above-average valuation — but not any valuation.

The questions to ask before concluding

Is ROIC above the cost of capital?

Has it been high for several years, or just the last one?

Is it stable, rising, or falling?

Can the company reinvest at that level of return?

Does the sector allow that return to last?

Can competitors easily attack those profits?

Is the number distorted by one-off items?

Is the company under-investing in its future?

Does the valuation still leave a margin of safety?

Bottom line

ROIC is, in my view, one of the best indicators for understanding the economic quality of a business. It measures how well a company turns invested capital into operating profit — and when it stays durably above the cost of capital, the company is creating value.

A strong ROIC can reveal a competitive advantage, good capital allocation, a profitable business, and disciplined management. Paired with room to grow, it can become a powerful engine of long-term returns.

But never use it in isolation: compare it to WACC, track it over several years, place it in its sector, understand what drives it, and check it isn’t resting on temporary or accounting effects.

For a beginner, one takeaway is enough:

A company shouldn’t just make money — it should make enough money relative to the capital it uses.

That’s exactly what ROIC measures. Not a final answer, but a valuable compass for telling apart the companies that consume capital from those that genuinely create value.

Want to get The Yield Dealer’s Newsletter in your inbox? Join other readers here.

Want short ideas on living and working on your own terms? Follow me on X/Twitter and Instagram.