The Most Boring Dividend Stock I’m Buying While Everyone Chases AI

💎 July 2026 Dividend Pick

ADP has raised its dividend for 51 straight years, trades well below its highs, and may be exactly the kind of boring compounder this market is ignoring.

Every month, I pick one dividend stock and buy it.

No timing games.

No macro predictions.

No chasing whatever ticker is trending on X this week.

The goal is simple: build a portfolio of businesses that can survive recessions, grow cash flow, raise dividends, and quietly compound for years.

This month’s pick is one of the least exciting companies I’ve ever written about.

It does not build chips.

It does not launch rockets.

It does not promise to “change the world with AI.”

It does not have a charismatic founder posting cryptic one-liners at 2 a.m.

It pays people’s salaries.

And that is exactly why I like it.

This month’s pick is Automatic Data Processing.

Ticker: ADP.

A company that has raised its dividend for 51 consecutive years.

Not in theory.

Not during easy markets only.

Not when rates were low and everyone looked smart.

ADP kept raising its dividend through recessions, inflation scares, financial crises, and the 2020 shutdown.

Fifty-one years.

Fifty-one raises.

Zero exceptions.

And right now, the stock is trading meaningfully below where it sat a year ago, while the underlying business continues to grow earnings, expand margins, and return capital to shareholders.

That is the kind of setup I like.

The Quick Thesis

Here is the entire ADP thesis in one box:

Company: Automatic Data Processing

Ticker: ADP

Business: Payroll, HR software, tax compliance, benefits administration

Dividend streak: 51 consecutive years of increases

Current yield: roughly 2.7–3.2%, depending on price

Most recent dividend raise: +10.4%

Main moat: switching payroll providers is painful, risky, and expensive

Hidden advantage: ADP earns interest income on client funds before payroll is distributed

Main risk: AI-driven headcount reduction could pressure employee-based revenue

My view: not a screaming bargain, but a high-quality dividend compounder trading at a fair-to-attractive price

This is not the kind of stock that makes people feel smart at dinner.

That is usually a good sign.

Why ADP?

Strip away the ticker, the ratios, and the financial jargon, and ADP’s job is almost embarrassingly simple:

It helps companies pay their employees correctly.

Payroll calculation.

Tax withholding.

Benefits administration.

HR software.

Labor law compliance.

Reporting across multiple states, countries, and jurisdictions.

When you get paid, there is a real chance ADP is part of the invisible machinery behind it.

The company serves clients across 140 countries and handles payroll for roughly 1 in every 6 U.S. workers.

It has been doing this since 1949.

Nobody gets excited about payroll software.

But the best businesses are often the ones people forget exist until they break.

And payroll is one of those things that absolutely cannot break.

A company can delay a marketing campaign.

It can postpone a software upgrade.

It can cut travel budgets.

It can pause hiring.

But it cannot casually fail to pay its employees.

That makes ADP boring.

It also makes ADP essential.

Why Payroll Is Stickier Than It Looks

Before I buy any business, I like to ask one simple question:

Can I explain, in one sentence, why a competitor cannot just show up next week and steal the customers?

For ADP, that sentence practically writes itself:

Switching payroll providers is such an operational nightmare that most companies avoid doing it unless they absolutely have to.

Think about what payroll actually touches.

Employee data.

Tax filings.

Benefits.

Compliance.

Time tracking.

HR workflows.

Accounting systems.

Internal approvals.

State and federal reporting.

Now imagine ripping all of that out and replacing it with a new provider.

For a small company, that is annoying.

For a company with thousands of employees across multiple states or countries, that is not a Tuesday afternoon project.

It is a multi-quarter operational risk.

And the person approving that switch is effectively saying:

“Let’s change the system that pays our entire workforce and hope nothing goes wrong.”

That is not a risk most executives volunteer for.

This is why ADP’s business is sticky.

Not because customers love payroll software.

Not because the product is flashy.

Not because the brand is cool.

Because once ADP is embedded, replacing it is painful.

That stickiness shows up in the numbers too: ADP’s client retention recently hit a record high.

The Second Moat: Regulatory Trust

There is another layer to ADP’s moat that investors often underrate.

Payroll law is not static.

It changes constantly.

And it changes differently depending on the state, country, industry, employee type, tax code, benefit structure, and reporting requirement.

Get it wrong, and the client may face penalties, employee complaints, tax issues, or legal headaches.

That is why companies are not simply shopping for the cheapest payroll tool.

They are shopping for trust.

They want the provider that knows the rules, updates the system, files the paperwork, and keeps them out of trouble.

That kind of trust is not built in a weekend.

It is not created by a slick AI demo.

It is not bought with venture funding.

It is not instantly replicated by a startup with a better interface.

ADP has spent decades building payroll data, compliance infrastructure, customer relationships, and institutional knowledge.

That is the kind of moat I like.

Not loud.

Not sexy.

But very hard to break.

The AI Question

Now let’s address the obvious bear case.

What if AI kills jobs?

ADP’s revenue is tied, in part, to the number of employees on its clients’ payrolls. Management tracks this through a metric called pays per control, which essentially measures how many people are being paid within ADP’s client base.

So if AI causes major headcount reductions across the economy, ADP could feel pressure.

That is a real risk.

I do not want to pretend otherwise.

But here is the more interesting wrinkle:

In the near term, AI may actually make payroll and compensation more complicated, not less.

New pay-transparency rules.

More complex compensation structures.

Hybrid workforces.

Cross-border employment.

Faster-changing regulation.

Performance-based pay.

AI-assisted HR decisions that require oversight and compliance.

All of this creates more complexity.

And complexity is good for ADP.

That is partly why ADP acquired Pequity in October 2025, a compensation-management software platform focused on pay analytics and compensation workflows.

That is not a company sitting still and waiting to be disrupted.

That is a company expanding deeper into the messy parts of HR and compensation.

Still, I am watching this risk closely.

If AI-driven headcount reduction becomes faster and deeper than expected, ADP’s employee-based revenue model could face pressure.

For now, I see AI less as an immediate existential threat and more as a force that may increase the need for trusted payroll, compensation, and compliance infrastructure.

But this is the key long-term risk in the thesis.

What the Financials Say

Now for the part that matters most:

ADP is not just a safe dividend story.

The business is still growing.

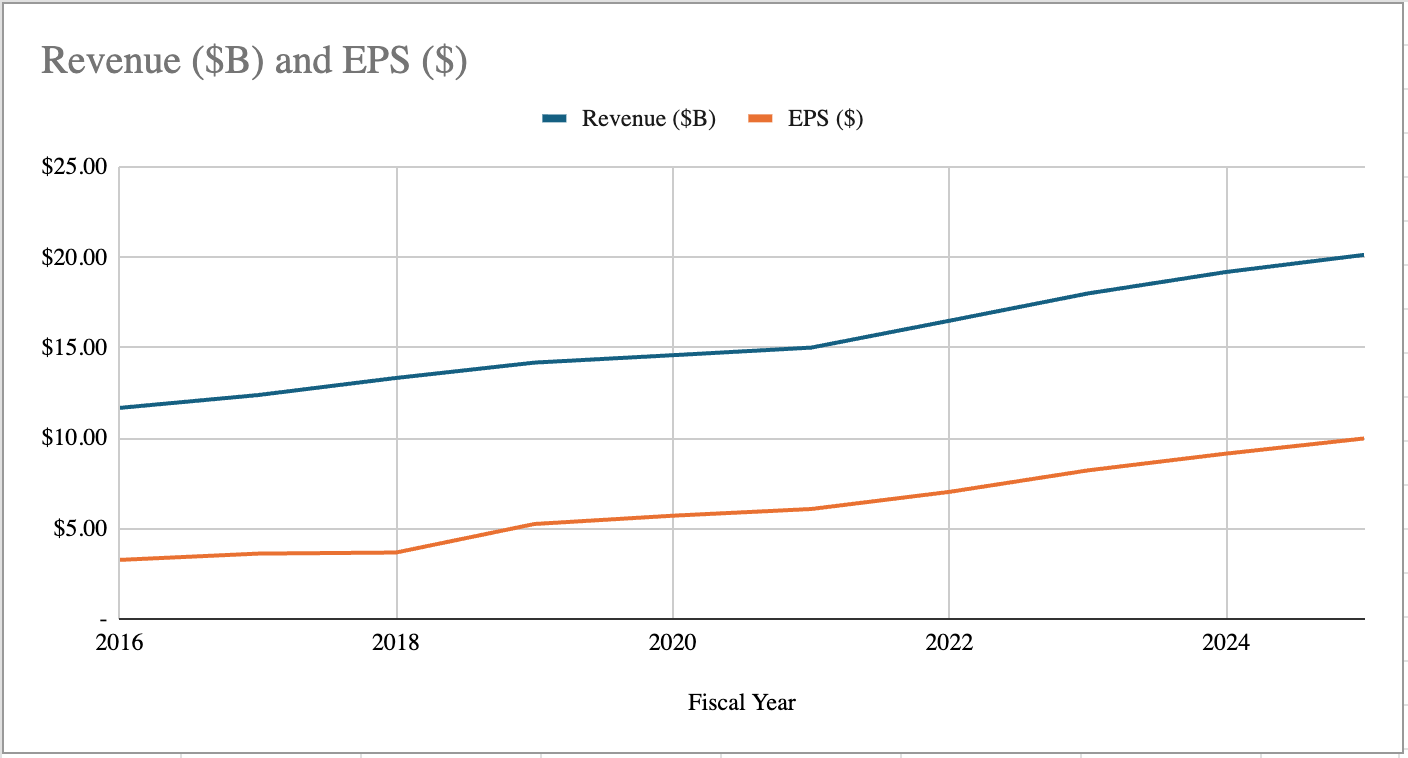

In its most recent quarter, ADP reported:

Revenue: $5.94 billion, up 7% year-over-year

Adjusted EPS: $3.37, up 10% year-over-year

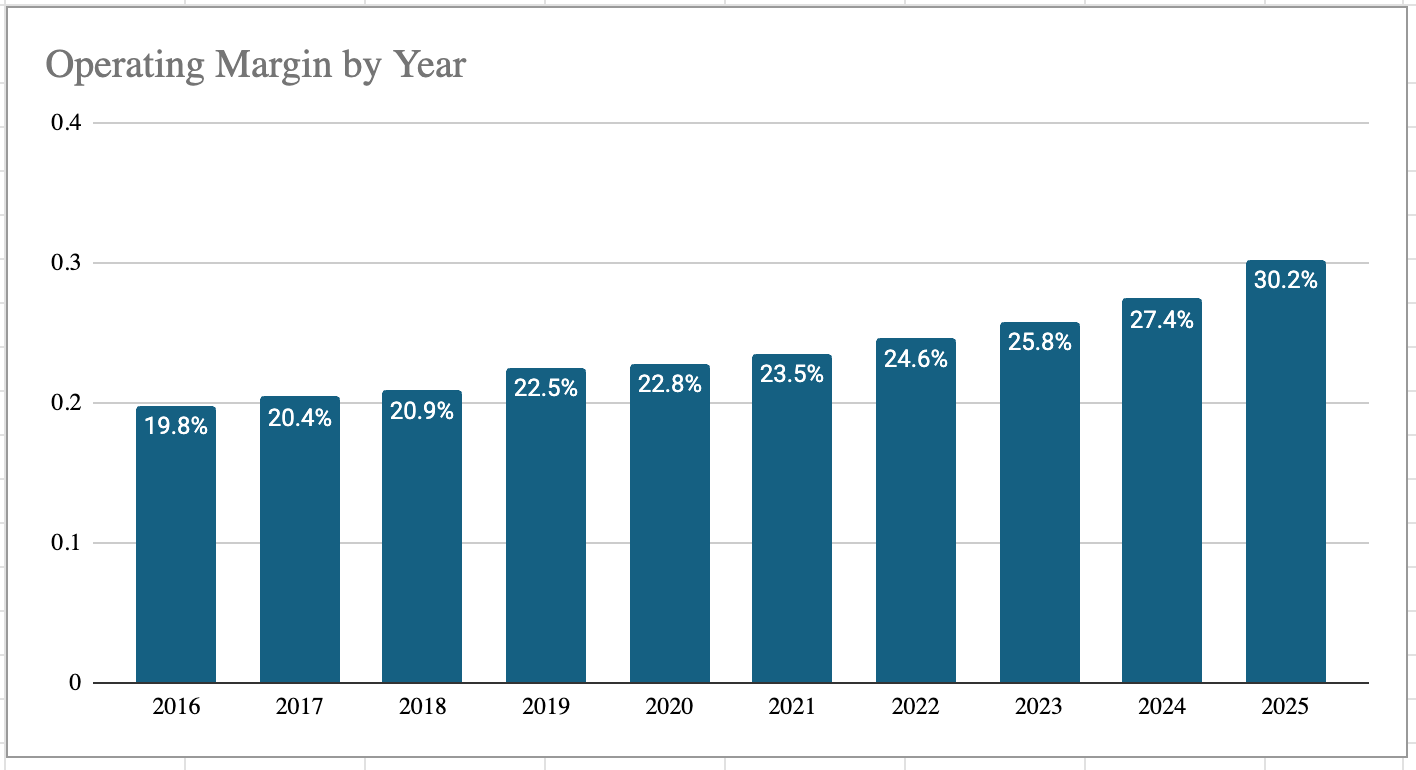

Adjusted operating margin: 30.2%

Guidance: raised for the full year

That last point matters.

This is not a company asking investors to wait for a turnaround.

It is already executing.

Revenue is growing.

Earnings are growing faster than revenue.

Margins are expanding.

Management is raising guidance.

That is exactly what you want to see from a mature compounder.

For the full fiscal year, ADP is expected to generate roughly $21.8–22.0 billion in revenue and more than $11 in adjusted EPS.

Again, this is not explosive growth.

It is not supposed to be.

This is a large, mature, asset-light business that keeps getting slightly more efficient over time.

That is the magic.

A business like ADP does not need to double overnight.

It just needs to keep adding clients, retaining clients, expanding margins, raising prices modestly, buying back stock, and increasing the dividend.

Do that for long enough, and the results become very powerful.

The Hidden Float Business Inside ADP

Here is one of the most underrated parts of the ADP story.

ADP holds a huge amount of client funds before those funds are distributed as payroll.

Think of it like this:

A company sends money to ADP.

ADP processes payroll.

Then that money is paid out to employees, tax authorities, and benefit providers.

During that short window, ADP is holding client cash.

And that cash can generate interest income.

ADP holds roughly $48 billion in average client funds.

In one quarter alone, that produced more than $400 million in interest income, up 14% year-over-year.

This is not the core payroll business.

It is an additional revenue stream layered on top of the core payroll business.

The closest analogy is insurance float.

An insurer collects premiums before it pays claims.

ADP receives client payroll funds before it distributes them.

In both cases, the company can earn income on the float in the meantime.

Of course, this has a downside.

If interest rates fall meaningfully, that income stream can shrink.

But as part of the overall business model, it is a quietly powerful advantage.

And most investors barely talk about it.

The Dividend: The Real Reason I’m Buying

Now let’s get to the reason ADP belongs in a dividend portfolio.

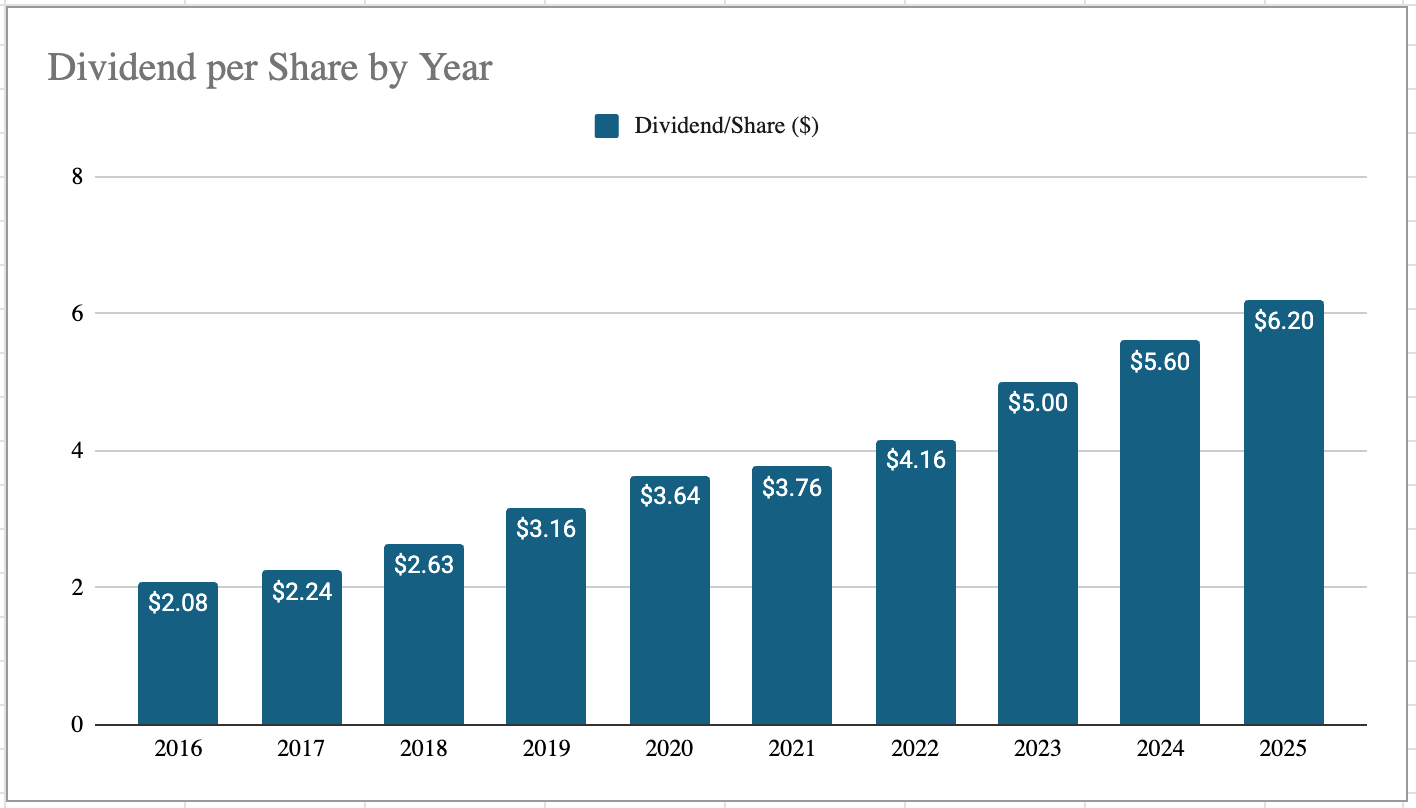

ADP has raised its dividend for 51 consecutive years.

That makes it a Dividend King.

The current annualized dividend is $6.80 per share, or $1.70 per quarter.

At recent prices, that puts the yield around 2.7–3.2%, depending on the exact share price you use.

That yield alone will not make anyone rich.

But the growth is what matters.

ADP’s most recent dividend increase was 10.4%.

Its 5-year dividend growth rate is roughly 12%.

The payout ratio sits around 59–62% of earnings, and free cash flow comfortably covers the dividend.

That is the combination I want:

A decent starting yield.

A long dividend growth record.

A manageable payout ratio.

Strong free cash flow.

A business that still grows earnings.

The mistake many income investors make is chasing the highest current yield.

A 5% yield looks attractive today.

But if that dividend barely grows, or worse, gets cut, the math quickly breaks down.

A 2.8% yield growing at 10% per year can become far more powerful over time than a static 5% yield going nowhere.

That is the kind of compounding I want.

Patient.

Boring.

Reliable.

Quietly devastating over long periods.

Very ADP.

Capital Returns Beyond the Dividend

ADP is not only returning cash through dividends.

The company has also repurchased roughly $1.46 billion of stock year-to-date.

Buybacks are not automatically good.

They only create value when a company buys back shares at reasonable prices and does not damage the balance sheet to do it.

In ADP’s case, I am comfortable with the capital return picture.

The dividend is covered.

The payout ratio is not stretched.

Free cash flow is strong.

The balance sheet is not being abused.

The company is still investing in growth areas like compensation analytics.

That is what good capital allocation looks like.

Not flashy.

Disciplined.

Valuation: Good, Not Perfect

Now let’s be honest about valuation.

ADP is not a dirt-cheap stock.

This is not a deep-value cigar butt trading at half of liquidation value.

It is a high-quality compounder trading at what I would call a fair-to-attractive price.

That distinction matters.

The stock has fallen meaningfully from its 52-week highs, but a lower stock price does not automatically mean a stock is cheap.

So I want to look at the valuation with the full range in mind.

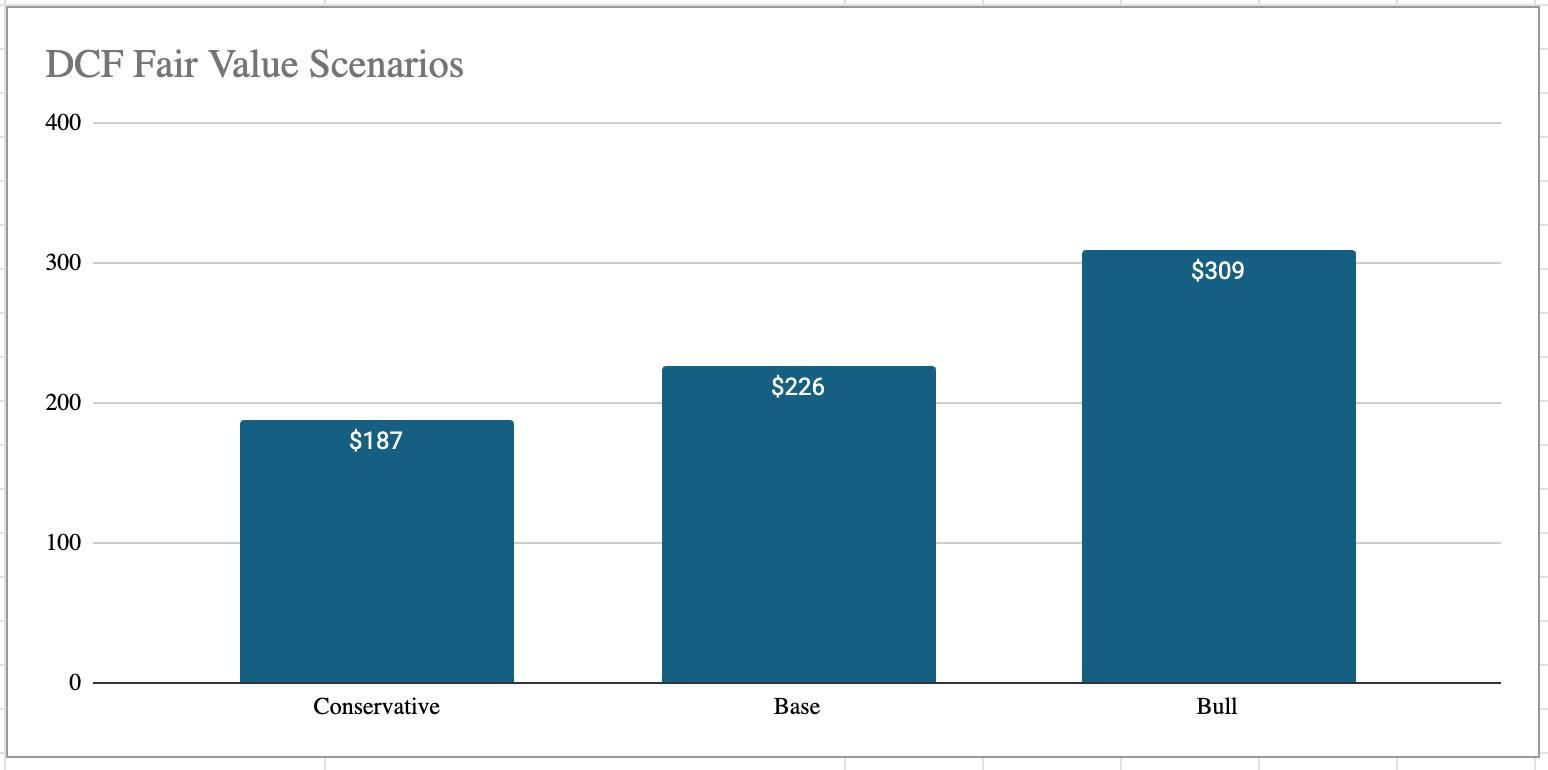

Based on Alpha Spread’s DCF scenario work:

What It Implies

Conservative case ~$187 - Stock looks expensive

Base case~$226 - Stock is slightly above fair value

Bull case~$309 - Stock offers roughly 23% upside

This is where the analysis gets interesting.

If you only use the bull case, ADP looks clearly undervalued.

If you use the base case, ADP looks close to fair value.

If you use the most conservative DCF assumptions, ADP looks expensive.

Same business.

Same model.

Different assumptions.

That is why valuation is never as clean as a single number.

Personally, I am leaning closer to the bull case than the conservative case.

Not because I want the higher number to be true.

Because the evidence currently supports a more optimistic interpretation:

Margins are expanding.

Management raised guidance.

Revenue is still growing.

Dividend growth remains strong.

Client retention is high.

ADP is expanding into more complex compensation workflows.

The business remains deeply embedded in client operations.

That does not guarantee a $309 fair value.

But it makes the bull case more credible than a fantasy scenario.

My conclusion:

ADP is not a screaming bargain. But it is a phenomenal business trading at a price where long-term investors can still win.

And for a Dividend King with this kind of moat, I do not need perfection.

I need a fair price, durable growth, and a dividend that can keep compounding.

ADP gives me that.

What Could Go Wrong?

No stock is risk-free.

Here are the main risks I am watching.

1. AI-driven headcount reduction

If AI reduces white-collar employment faster than expected, ADP’s pays-per-control metric could come under pressure.

That is the biggest structural risk.

2. Interest rate sensitivity

ADP earns income on client funds. If interest rates fall meaningfully, that float income could decline.

This would not destroy the thesis, but it could create a temporary earnings headwind.

3. Valuation risk

ADP is a high-quality company, and the market knows it.

If growth slows, the stock could re-rate lower.

This is not a stock where I want to massively overpay.

4. Competition

Paychex, Workday, Paylocity, and other HR/payroll platforms are not standing still.

ADP’s size and reputation are advantages, but the market remains competitive.

None of these risks break the thesis for me today.

But they are the things I will monitor every quarter.

My Decision